Pricing

Coupon Calendar

Coupon Schedules

Cash Calculator

Guide

Open main menu

Home

Guide

Guide

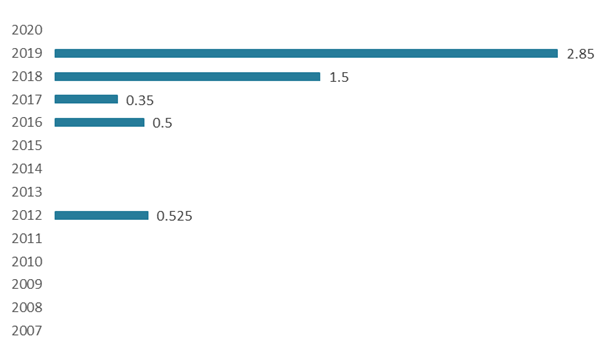

Redemptions

What amount has been redeemed by Nigerian issuers?

Total:

$5.725 billion

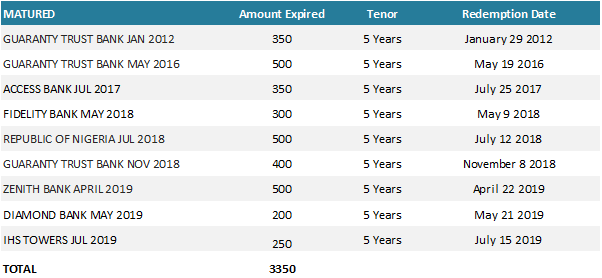

Which Nigerian Eurobonds have matured?

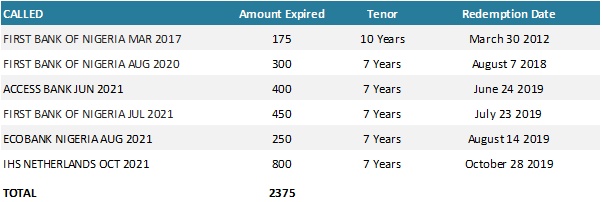

Which Nigerian Eurobonds have been called?

Next page: Basics

Thoughts, comments, suggestions?

We'd love to hear from you.

Contact Us